The ANDA Threat Landscape in 2026: What Brand Pharma Needs to Know

By Steve Ouellette

TL;DR

-

Generic challengers are filing broadly and aggressively. As of January 2026, the FDA's Paragraph IV list contains 1,588 entries across 880 drugs. Drugs approved as recently as 2021 are already facing multiple generic challenges years before their patents expire, and revenue alone does not predict which drugs get targeted.

-

Patent thicket size alone is not a deterrent. Analysis of the top 100 most-targeted drugs found no correlation between the size of a patent portfolio and the number of generic challengers. Meanwhile, compounding and regulatory shifts are creating competitive pressures that bypass the defenses from patents.

-

Preparation is the differentiator. The brand teams that navigate this landscape successfully are the ones monitoring early, stress-testing their patent portfolios, and building cross-functional response plans before the Paragraph IV notice arrives.

The Patent Super-Cliff Is Here

The pharmaceutical industry is entering what analysts have called a "patent super-cliff." Over $200 billion in branded drug sales are exposed to generic competition through 2030, and Paragraph IV ANDA filings, a primary legal mechanism for generic market entry, continue at a steady pace. As of January 2026, the FDA's Paragraph IV Certification List contains 1,588 entries spanning 880 unique drugs, each representing a generic applicant's assertion that the brand's patents are either invalid or will not be infringed.

For brand-side pharmaceutical teams, each Paragraph IV filing triggers a cascade of strategic decisions, from patent litigation and lifecycle management to commercial readiness planning. The companies that navigate this period successfully will be the ones that see these challenges coming early and respond with discipline.

This post examines the current ANDA filing landscape using FDA data through January 2026 and outlines the strategic considerations that should inform any brand's response. The analysis represents a strategic review of publicly available data from the FDA, patent filing data, SEC filings, and other relevant press releases as part of an ongoing effort to better understand how generic entry timing is evolving. While detailed patent vulnerability analysis requires product-specific legal review, the aggregate trends suggest that even recently approved products face substantial generic interest, settlement appears increasingly central, and patent quantity alone does not deter filings.

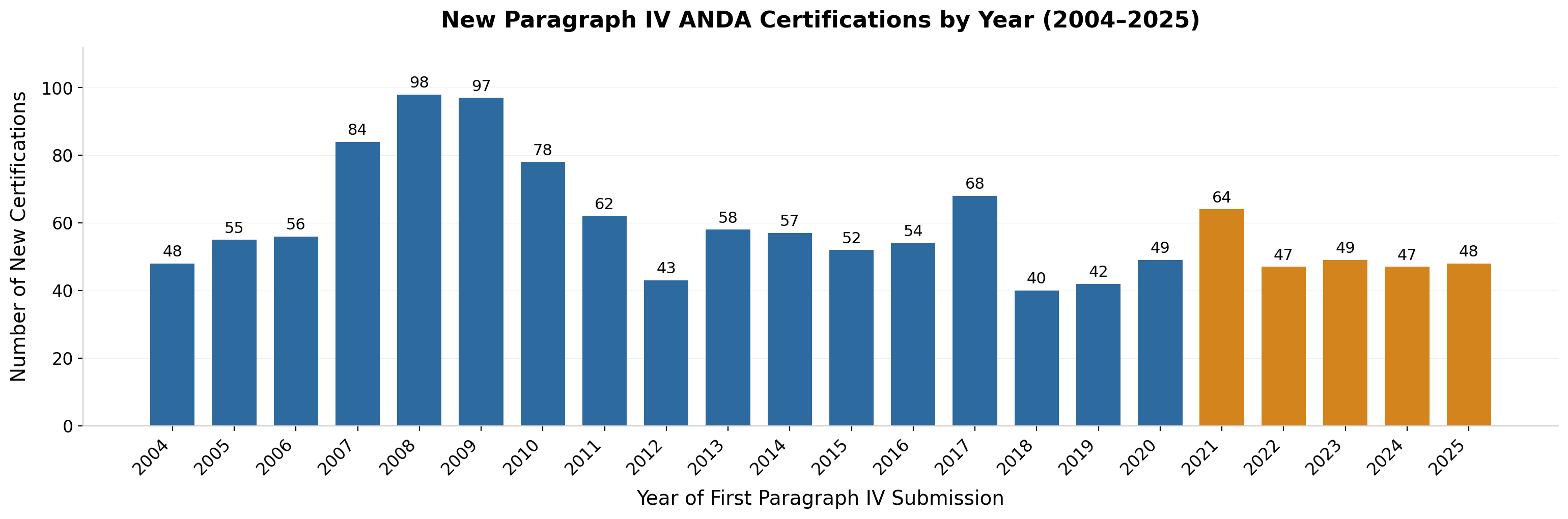

Figure 1: New Paragraph IV ANDA Certifications by Year (2004-2025). Source: FDA Paragraph IV Certification List, January 2026 update. Excludes 242 pre-MMA entries. Each bar represents unique drug/strength combinations receiving first PIV certification that year.

Figure 1: New Paragraph IV ANDA Certifications by Year (2004-2025). Source: FDA Paragraph IV Certification List, January 2026 update. Excludes 242 pre-MMA entries. Each bar represents unique drug/strength combinations receiving first PIV certification that year.

Where the Pressure Is Building

The Most-Targeted Drugs

Not all ANDA activity is created equal. While 880 drugs appear on the Paragraph IV list, generic interest concentrates unevenly and not always where you might expect. Among drugs with patents expiring after 2026, the most targeted brands have drawn dozens of individual ANDA filings, each essentially a bet placed by a generics company that it can successfully challenge the innovator's patent portfolio or reach a favorable settlement. Revenue matters in the decision to file an ANDA, but it is far from the only factor driving these decisions.

Table 1: Most-Targeted Drugs by Paragraph IV Filings (Patent Expiry After 2026)

| Drug (Brand) | Therapeutic Area | 2024 Revenue | ANDAs Filed | Last Patent Expiry |

|---|---|---|---|---|

| Dimethyl Fumarate (Tecfidera) | Neurology; Relapsing MS | ~$1.0B | 29 | Feb 2028 |

| Apixaban (Eliquis) | Hematology; Atrial Fibrillation | $13.3B | 25 | Feb 2031 |

| Teriflunomide (Aubagio) | Neurology; Relapsing MS | ~$410M | 21 | Feb 2034 |

| Dapagliflozin (Farxiga) | Endocrinology; Type 2 Diabetes | $7.7B | 20 | May 2030 |

| Efinaconazole (Jublia) | Dermatology; Onychomycosis | N/D | 19 | Oct 2034 |

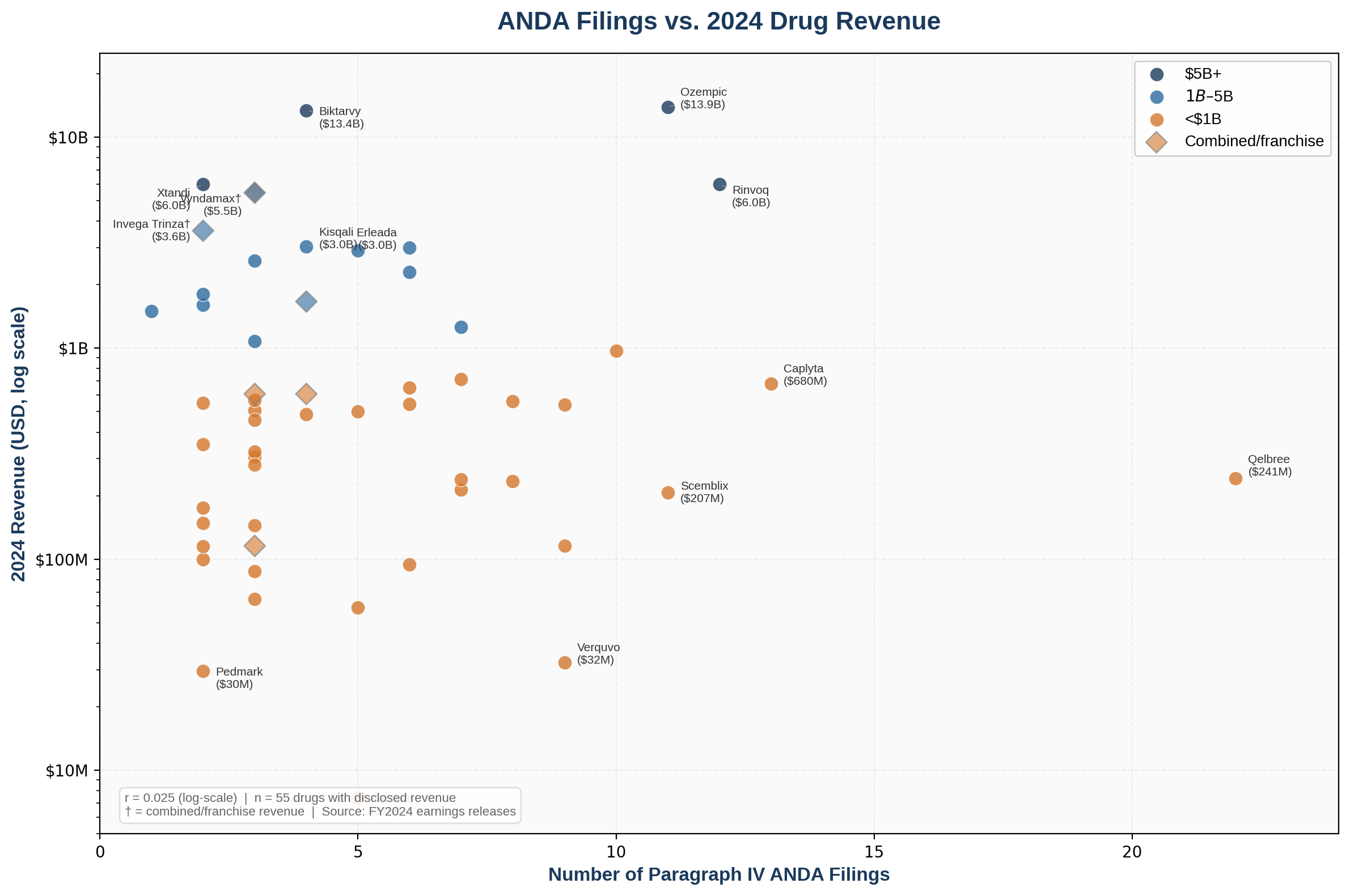

Figure 2: ANDA Filings vs. 2024 Drug Revenue (log scale). Revenue alone is a poor predictor of generic filing activity. Other factors, including patent vulnerability and therapeutic area dynamics, play a significant role.

Figure 2: ANDA Filings vs. 2024 Drug Revenue (log scale). Revenue alone is a poor predictor of generic filing activity. Other factors, including patent vulnerability and therapeutic area dynamics, play a significant role.

The top of the table is dominated by high-revenue drugs with broad patient populations; Eliquis at $13.3 billion in 2024 global sales has drawn 25 separate ANDA filings, and Tecfidera leads with 29. But revenue alone does not reliably predict the volume of generic challenges. The analysis did not identify a correlation between the number of ANDA filings for a given drug and its 2024 revenue. Several billion-dollar products have attracted only a handful of filings, while mid-tier drugs like Qelbree ($241M) and Caplyta ($681M) have drawn 8 and 7, respectively. Generic companies are clearly evaluating more than market size. Patent vulnerability, competitive positioning, and the feasibility of the challenge all factor into the decision to file.

Recently Approved Drugs Are Not Immune

One assumption that brand teams should not rely on is that a recently approved drug will enjoy years of uncontested market exclusivity before generic interest materializes. Among drugs approved in the last five to eight years, several have already attracted substantial Paragraph IV filing activity, with challenges arriving well before their patents expire.

Table 2: Most-Filed Paragraph IV ANDAs (January 2021 - January 2026)

| Drug (Brand) | Therapeutic Area | FDA Approval | First Para IV Filing | 2024 Revenue | ANDAs Filed | Last Patent Expiry |

|---|---|---|---|---|---|---|

| Selenious Acid | Nutrition; Parenteral Supplementation | Apr 2019 | Jun 2024 | N/D | 11 | Jul 2041 |

| Cannabidiol (Epidiolex) | Neurology; Epilepsy | Jun 2018 | Sep 2022 | $972M | 10 | Mar 2041 |

| Bempedoic Acid (Nexletol) | Cardiology; Dyslipidemia | Feb 2020 | Feb 2024 | $116M | 9 | Jun 2040 |

| Elagolix (Orilissa) | OB/GYN; Endometriosis | Jul 2018 | Jul 2022 | N/D | 9 | Sep 2036 |

| Finerenone (Kerendia) | Nephrology; CKD | Jul 2021 | Jul 2025 | $540M | 9 | Jul 2035 |

| Viloxazine HCl (Qelbree) | Psychiatry; ADHD | Apr 2021 | Apr 2025 | $241M | 8 | Apr 2035 |

| Voclosporin (Lupkynis) | Rheumatology; Lupus Nephritis | Jan 2021 | Jan 2025 | $235M | 8 | Dec 2037 |

| Lumateperone (Caplyta) | Psychiatry; Schizophrenia | Dec 2019 | Dec 2023 | $681M | 7 | Dec 2040 |

| Semaglutide (Ozempic/Wegovy) | Endocrinology; Type 2 Diabetes/Obesity | Dec 2017 | Dec 2021 | $33.8B* | 7 | 2027-2041 |

Key insight: If your product was approved in the last five years and has significant revenue potential, the question is not whether generics will challenge your patents, it is how many have already filed.

*Combined global revenue for Ozempic, Wegovy, and Rybelsus. N/D = not separately disclosed by manufacturer.

Viloxazine (Qelbree), approved in 2021 for ADHD, has already attracted 8 unique generic challengers despite patents extending to 2035. Lumateperone (Caplyta) and Finerenone (Kerendia) show the same pattern. Generic companies are filing challenges years in advance, positioning themselves for first-to-file exclusivity and signaling to the market that they view these patents as vulnerable.

The 180-Day Exclusivity Backlog

The 180-day exclusivity provision is the prize that motivates first-to-file Paragraph IV applicants, but is showing signs of strain. Analysis of the January 2026 Paragraph IV list reveals that roughly 35% of entries still have a pending 180-day exclusivity status determination. Of those, about 26% are eligible for exclusivity, 24% have had their exclusivity extinguished, and 8% are deferred.

This backlog creates strategic uncertainty for all parties. Generic applicants cannot be sure of their exclusivity position, while brand companies face difficulty predicting when, and how many, generic competitors will actually reach the market. Adding to the complexity, even a first-filer that secures 180-day exclusivity may find the prize diminished: brand companies can launch an authorized generic during the exclusivity period, and industry data suggests that authorized generics reduce a first-filer's revenue during exclusivity by 40-50%. For brand teams, this dynamic underscores the importance of monitoring not just the number of ANDA filings but also the exclusivity status of each applicant, and having an authorized generic strategy ready to deploy.

Why Patents Alone Won't Protect You

Patent Thickets: More Isn't Always Better

Building a large patent portfolio around a drug, often referred to as a "patent thicket", has become a standard defensive strategy. However, analysis of the top-targeted drugs reveals the size of a patent portfolio does not reliably deter generic challenges.

Table 3: Patent Portfolio Size vs. ANDA Filing Volume

| Drug (Brand) | Orange Book Patents | Paragraph IV ANDAs |

|---|---|---|

| Upadacitinib (Rinvoq) | 44 | 5 |

| Cannabidiol (Epidiolex) | 32 | 10 |

| Lumateperone (Caplyta) | 25 | 7 |

| Semaglutide (Ozempic) | 19 | 7 |

| Viloxazine (Qelbree) | 6 | 8 |

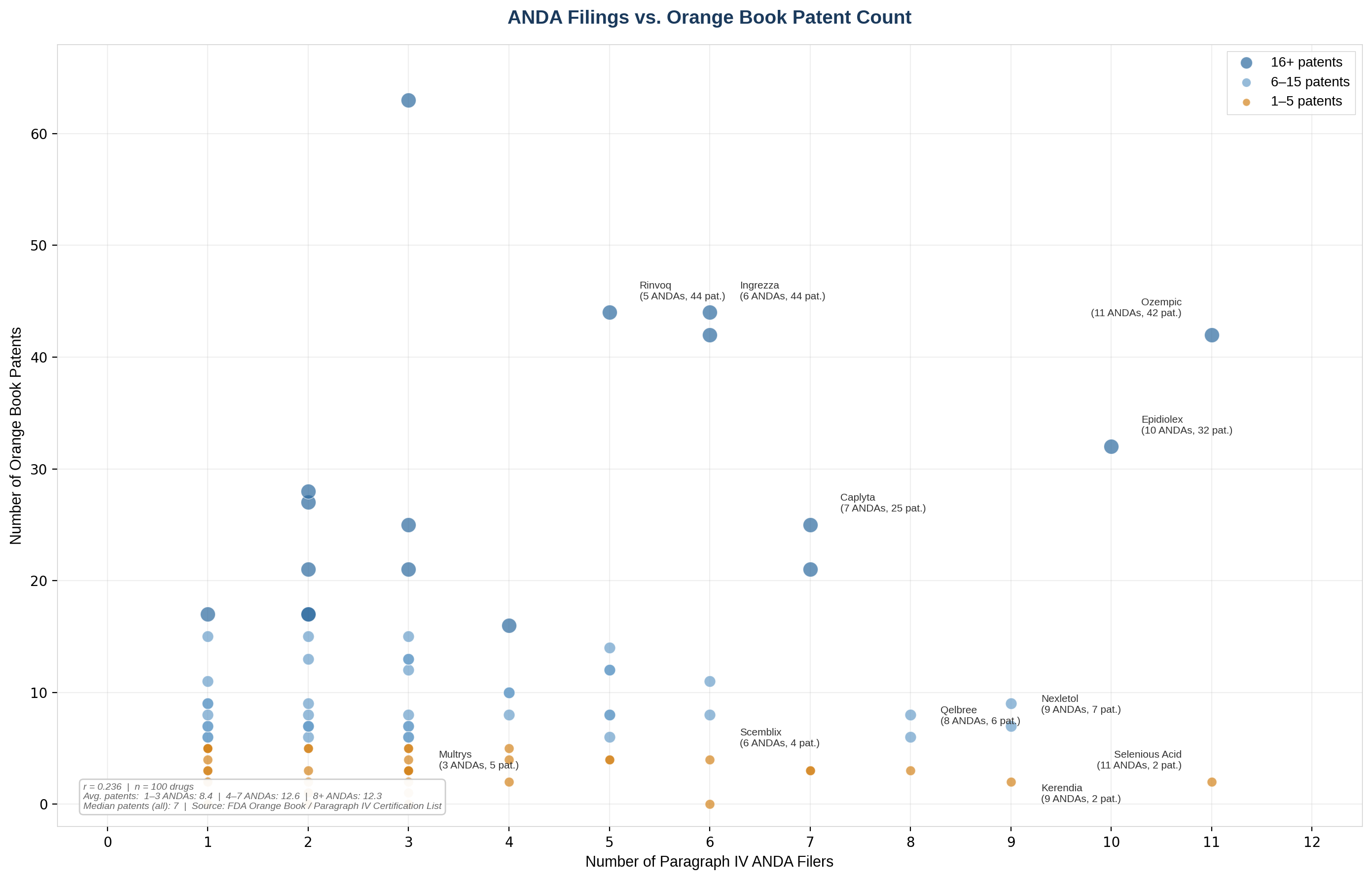

Upadacitinib's 44 Orange Book patents have attracted 5 unique challengers; Viloxazine's 6 patents have attracted 8. While a larger portfolio can increase the cost and complexity of a generic challenge, it is not a reliable proxy for deterrence. Generic companies evaluate patent quality including the breadth of claims and the likelihood of surviving validity challenges more than sheer quantity. A generic product may only need to get around a small subset of all the granted claims in the patent thicket to confidently have freedom-to-operate.

Figure 3: ANDA Filings vs. Orange Book Patent Count. Patent portfolio size shows no consistent relationship with the number of generic challenges filed.

Figure 3: ANDA Filings vs. Orange Book Patent Count. Patent portfolio size shows no consistent relationship with the number of generic challenges filed.

This has implications for patent strategy. Resources spent building a large but weak portfolio might be better invested in fewer, higher-quality patents with broad claims and strong prosecution histories.

Regulators are taking notice. In 2023, the FTC sent letters to 14 pharmaceutical companies challenging over 400 improperly listed Orange Book patents, a direct signal that bloated patent portfolios are drawing enforcement scrutiny in addition to failing to deter generics. Meanwhile, a structural weakness in the Orange Book itself compounds the problem: the "use codes" that brands submit to describe what their patents cover are limited to just 250 characters, arising from a constraint rooted in an FDA database field size, not in any patent law principle. That limitation creates ambiguity that can be exploited during listing and makes portfolios more vulnerable to regulatory and legal challenge.

Semaglutide: A Case Study in Converging Pressures

Semaglutide, the active ingredient in Novo Nordisk's Ozempic, Wegovy, and Rybelsus weight loss franchise, is a recent example that illustrates three simultaneous pressures: early ANDA challenges, managed litigation settlements, and opportunistic compounding. With 7 unique generic challengers and a patent estate spanning from 2027 to 2041, semaglutide has become a case study in how brand and generic companies negotiate the path to market entry.

In late 2024, Novo Nordisk settled patent litigation with several major generic companies that filed ANDA applications, including Mylan, Dr. Reddy's, Apotex, and Sun Pharmaceuticals. The terms are confidential, but industry observers expect managed generic entry in the U.S. around 2031-2032, after the extended compound patent expires. Meanwhile, international markets are moving faster, with generic semaglutide expected in Canada, India, and Brazil as early as 2026, following patent lapses and regulatory developments in those jurisdictions.

Novo Nordisk also encountered threats from competitors taking advantage of opportunities for market entry due to drug shortages. For high demand drugs that make it onto the FDA shortage list, the door to compounding is opened and can sometimes persist even after supply stabilizes. During the multi-year shortage of Novo Nordisk's Ozempic and Wegovy, compounding pharmacies and telehealth platforms capitalized on a regulatory exception that permits compounding of drugs on the FDA's shortage list. By Novo Nordisk's own estimate, as many as 1.5 million Americans were using compounded GLP-1 drugs by early 2026. Even after the FDA resolved the semaglutide shortage in February 2025, compounders were slow to exit the market. The situation escalated dramatically this month when Hims & Hers Health launched a compounded oral semaglutide pill at $49 per month, a fraction of the branded Wegovy pill's $149 self-pay price. The response was swift and coordinated: within 24 hours, FDA Commissioner Martin Makary pledged "decisive steps" against companies mass-marketing unapproved GLP-1 copies, and the Department of Health and Human Services referred Hims & Hers to the Department of Justice for potential violations of federal law. Hims pulled the product within two days, but Novo Nordisk followed through with a patent infringement lawsuit filed in the U.S. District Court for the District of Delaware, alleging willful infringement of its semaglutide patent, which extends through 2032, and seeking damages that could reach hundreds of millions of dollars.

The semaglutide case demonstrates that brand owners must consider a full arsenal of strategies for managing the timeline for generic entry. This includes thoughtful planning around patent protection, preparing for negotiations to settle with ANDA filers, and awareness of compounding channels.

Regulatory and Legislative Headwinds

Several regulatory and legislative developments are worth watching closely. In October 2025, the FDA launched an ANDA Prioritization Pilot that gives review preference to applications involving domestic API manufacturing. Given that only about 9% of active pharmaceutical ingredient manufacturers serving the U.S. market are domestically based, this pilot could meaningfully reshape which ANDAs reach approval first and alter the competitive dynamics for brands whose generic challengers rely on overseas supply chains.

Recent years have also seen a wave of legislation aimed at removing barriers to generic competition:

- The CREATES Act (2019) gave generic companies the legal right to sue for access to branded drug samples needed for bioequivalence testing, addressing a known brand-side tactic of withholding samples to delay ANDA filings;

- The Orange Book Transparency Act (2020) now requires brands to delist invalidated patents within 14 days of a court decision, reducing the window for expired or invalidated patents to block generic approvals;

- The BLOCKING Act (2025), if enacted, would modify the 180-day exclusivity framework to allow entry of a second generic if a company with the first generic "parks" or "holds" release of their approved generic as part of a deal with the branded drug's owner; and

- The Stop STALLING Act (2025) targets sham citizen petitions, used to delay generic approval, by imposing stricter requirements on the FDA's review process for petitions filed near ANDA approval dates.

Together, these measures signal a clear legislative trend: the tools that brand companies have historically used to extend market exclusivity beyond patent expiry are being systematically curtailed.

Finally, brand teams should be aware that Paragraph IV filings are not the only source of competitive pressure. Pharmacy compounding under Sections 503A and 503B of the FD&C Act has emerged as a parallel channel, particularly for high-demand products during supply shortages. The semaglutide experience is instructive: while the drug was on the FDA's shortage list, 503B outsourcing facilities compounded and distributed semaglutide injections at scale. When the shortage resolved, FDA enforcement and Novo Nordisk's litigation campaign shut down most of that activity. Compounding is not a substitute for the ANDA pathway, but it can erode brand revenue in the short term and complicate commercial planning, especially for products facing both supply constraints and patent challenges.

The Brand-Side Playbook

Receiving a Paragraph IV certification notice is a pivotal moment, but it should not be the first time a brand team thinks about generic competition. Brand companies have a standard set of defensive tools available, but the most effective responses begin well before the notice arrives.

Defensive Tools

Brand companies have several established tools for responding to Paragraph IV challenges:

- Patent litigation and the 30-month stay. Filing suit within 45 days of receiving a Paragraph IV notice triggers an automatic 30-month stay of FDA approval, buying time for the brand to litigate. This remains the most commonly used first response.

- Product lifecycle management. New formulations, delivery systems, or indications can extend a product's commercial relevance even as generics enter the original market. Authorized generics, branded versions sold at generic pricing, can also capture share in the generic segment.

- Citizen petitions. Petitions to the FDA can raise legitimate scientific or regulatory concerns about a proposed generic, but as described above this tool has drawn increasing scrutiny from the agency and from legislators.

- Settlement negotiations. As the semaglutide example illustrates, negotiated settlements that establish a managed entry date are increasingly common. These agreements must, however, be carefully structured to avoid antitrust exposure.

A Four-Part Assessment Framework

Rather than reacting to Paragraph IV filings as they arrive, brand teams benefit from a structured, ongoing assessment of their generic vulnerability. The following framework provides a starting point.

1. Early Warning Monitoring

The FDA's Paragraph IV Certification List is updated regularly and is publicly available. Monitoring this list, Orange Book patent listings, ANDA approval activity, and patent litigation dockets provides early signals about generic interest in your products. The number of ANDAs filed against comparable drugs in your therapeutic area can also serve as a leading indicator.

2. Patent Portfolio Analysis

As the data above illustrates, the number of patents is less important than their quality and scope. A rigorous assessment should evaluate each patent's claim breadth, the strength of its prosecution history, its vulnerability to inter partes review, and whether it covers the most commercially relevant aspects of the product. Also consider "white space" in the patent thicket and workarounds a generic competitor might use to obtain freedom-to-operate.

3. Timeline Mapping

Generic entry rarely happens on a single date. It unfolds through a sequence of events: Paragraph IV filing, patent litigation, potential 30-month stay, 180-day exclusivity (if applicable), and final ANDA approval. Mapping these milestones for your product and for the generic applicants targeting it allows for more precise commercial planning and helps avoid the common trap of treating "patent expiry" as a single cliff event.

4. Cross-Functional Readiness

An effective ANDA response requires alignment across legal, regulatory, commercial, and supply chain teams. Patent litigation strategy, lifecycle management decisions, pricing adjustments, and supply planning all intersect. The brand teams that handle generic entry most effectively are those that have rehearsed these decisions before the pressure arrives.

Preparation, Not Panic

The ANDA landscape in 2026 is more active, more complex, and faster-moving than at any point in the past decade. Paragraph IV filings are reaching drugs well before their patents expire, including products approved within the last five years. Patent thickets are providing less deterrence than many brand teams assume, and regulatory changes are introducing new variables into an already complicated equation.

But none of this is cause for panic. The tools available to brand-side teams (litigation, lifecycle management, settlement, authorized generics, and proactive monitoring) are well established and effective when deployed with the right intelligence and timing. The difference between a well-managed generic entry and a disruptive one almost always comes down to preparation.

The first step is understanding your specific risk profile: how many ANDAs have been filed against your products, what your patent portfolio actually protects, and where your timeline vulnerabilities lie. That assessment is the foundation for every strategic decision that follows.

This analysis is based on publicly available FDA data through January 2026, including the Paragraph IV Certification List, Orange Book patent listings, ANDA approval records, SEC filings, case law, legislation, and relevant press releases. It is intended for informational purposes and does not constitute legal advice.

Need a custom competitive, IP, or diligence review for your team?

Solidus Bio delivers analyst-grade research for biotech companies and investors making high-stakes decisions.

Book a Scoping Call